"It Ain't What You Invest, It's The Way That You Do It - That's What Gets Results"

Hum the above to the tune of Bananarama's 1982 opus

Friend,

Towards the end of last year, I had the pleasure of being introduced to a potential new client couple. As always, they were referred to me by existing clients. This still gives me a thrill; please keep on thrilling me.

The couple - let's call them Melania and Donald - were at a transition point in their lives. In the middle of last year, Donald left BT, twenty years after joining its graduate entry program in 2003. Now, between roles and with plenty of gardening leave affording the couple time to think about stuff nobody ever wants to think about, they were aware that, in their early forties, it was time to properly plan for their future selves.

Sub-Optimal

The three of us sat down and did the collaborative financial planning with their lifetime cash flow forecast front and central. “By bringing their financial future into the present”, the cash flow showed some issues. Namely, if the two of them walked away from work on their terms, at their time of choosing and not the boss’s1, they were going to run out of money later on in life.

This is a distinctly sub-optimal outcome.

In such a situation, the easiest thing for an adviser to say is “You need to save more between now and retirement.” The rub? There’s only so much more people can save. Yes, cutbacks in lifestyle can be made, to find some extra dosh that can be salted away. But who wants to do that? Answer: nobody, in my two-decades plus experience in doing this work.

So, instead, here’s a thought: if you’re regularly saving and investing as much as you reasonably can (the “what”), focus instead on the way you’re investing those monthly savings. And this is what Melania, Donald and I did.

At some stage during his time at BT, Donald had enrolled in the company pension scheme. He had a million other things to be doing than paying heed to the underlying investment fund that he and his employer’s monthly contributions were going into. Turns out that Donald’s BT pension pot was invested in a low-return fund, one deliberately constructed to minimise volatility (and by definition, to minimise returns).

For a young investor saving for a retirement many decades away this is borderline criminal, but there you go.

Donald knew what he was investing in terms of pounds and pence; he had no idea how (the way) that money was being invested.

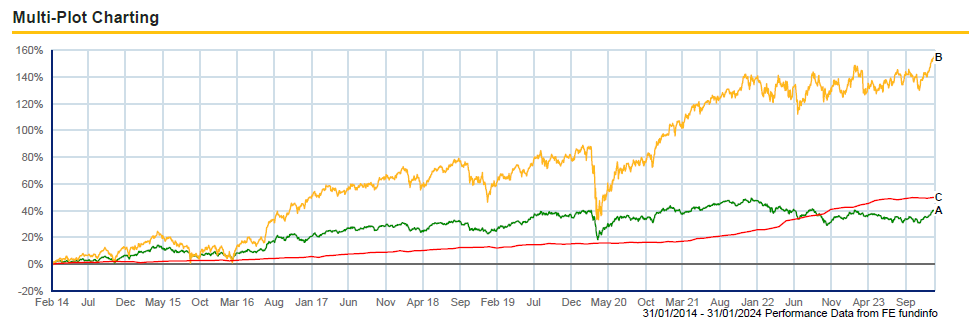

Sadly for Donald, his pension fund was (is) a complete pig. Over the 10 years to 1st February 2024, it grew by 39.6%, or just 3.4% a year2. In real, inflation-adjusted terms - the only terms that matter, ultimately - the pension fund delivered a negative return over that decade. This takes some doing!

Apples v Pears

By comparison, our preferred global equity fund, chock full of The Great Companies of The World (GCOTW), returned 9.9% per annum over that time. Is comparing Donald’s fund with this very much an apples and pears thing? Yes, and I’m fine with that; in catastrophic ignorance, way too many people are investing in “apples” when they should be in “pears”.

What if Donald had changed not “the what” but the way his pension pot was invested?

By way of example, let’s imagine that, over the last decade, Donald’s pension pot received £3,000 a month combined from him and BT. In that time, his Apple Pig Fund returns 3.4% a year. After 10 years, his pension pot is worth £429,266.

What if, back in early 2014, Donald had changed the way his pension fund was invested, to the GCOTW one referred to above? Let’s call this the Pear Salvation Fund. His £3,000 a month regular saving gives him a pension pot of £616,069 after 10 years.

That’s nearly £200,000 more in his pot after just one decade. He didn’t have to change what he was saving to get that; he just changed the way his pot was invested.

This is not cherry-picking the timeframe. Nothing spooks markets more than unanticipated events, of which, over the last 10 years, there have been many:

Brexit and the subsequent shenanigans

Orange Man Bad becomes US President

The Fauci-Flu/Wuhan Lab Leak

Around 14 Prime Ministers

Putin’s Ukrainian reclamation project

Double-digit inflation

The genocidal act of war on 7th October last year and the ongoing response

That’s enough bad news to keep the three-headed Cerberus that is KPR (Kuenssberg-Peston-Rigby) perpetually on our TV screens. Or so I’m told: I’ve barely watched a minute of “news” in well over a decade, and my therapist says I’m improving all the time3.

Yet despite the ongoing dramas that we dumb homo sapiens can’t but help create, the Great Companies of The World (GCOTW) have delivered inflation-busting returns.

What Really Gets Results

You can scour the internet and find the cheapest pension or ISA pot available. You can be salting away what you can afford every month into these tax-efficient wrappers. But the biggest determinant of the eventual size of these investments - and hence their use to you - will be the way they are invested, coupled with your ability to stick to the plan through thick and thin.

Thankfully we are reconfiguring Donald’s pension pot and completely revamping his investment mix (or “asset allocation”, as people with zero soul say) so that going forward he is 100% invested in the GCOTW.

We don’t have a time machine. We can’t go back a decade and start over. But at 43, Melania and Donald have a financial plan and an investment approach beautifully aligned with their plan. The couple still has time to get their financial future sorted, and sorted it will be; the universe has a way of looking after those who look after themselves.

The song remains the same: no portfolio without a plan, as Bananarama almost said.

An apostrophe nightmare. But I think one boss possessive is “boss’s”. Two or more bosses is “bosses’”. As you were.

All performance figures from Trustnet. Net of fund management fees, gross of advisory/custodial fees.

One of the limitless upsides to not watching the news is that I wouldn’t recognise Chris Whitty if I ran over him. And if I did recognise him, that’s exactly what I would do.

Excellent first article, Nick. I met with a client today who, unwittingly, is in a lifestyle fund within their workplace pension. She's 48, selected retirement age is 55. So it's already been 'de risking' from an already low base. Criminal really. Hence why our work is never done! Look forward to future musings! Dan.